When you want to buy a car, you have two funding options. You can choose between a Car Loan or a Car Lease. Here, we will discuss car loans, car leases and the details of both these methods.

Car Loan

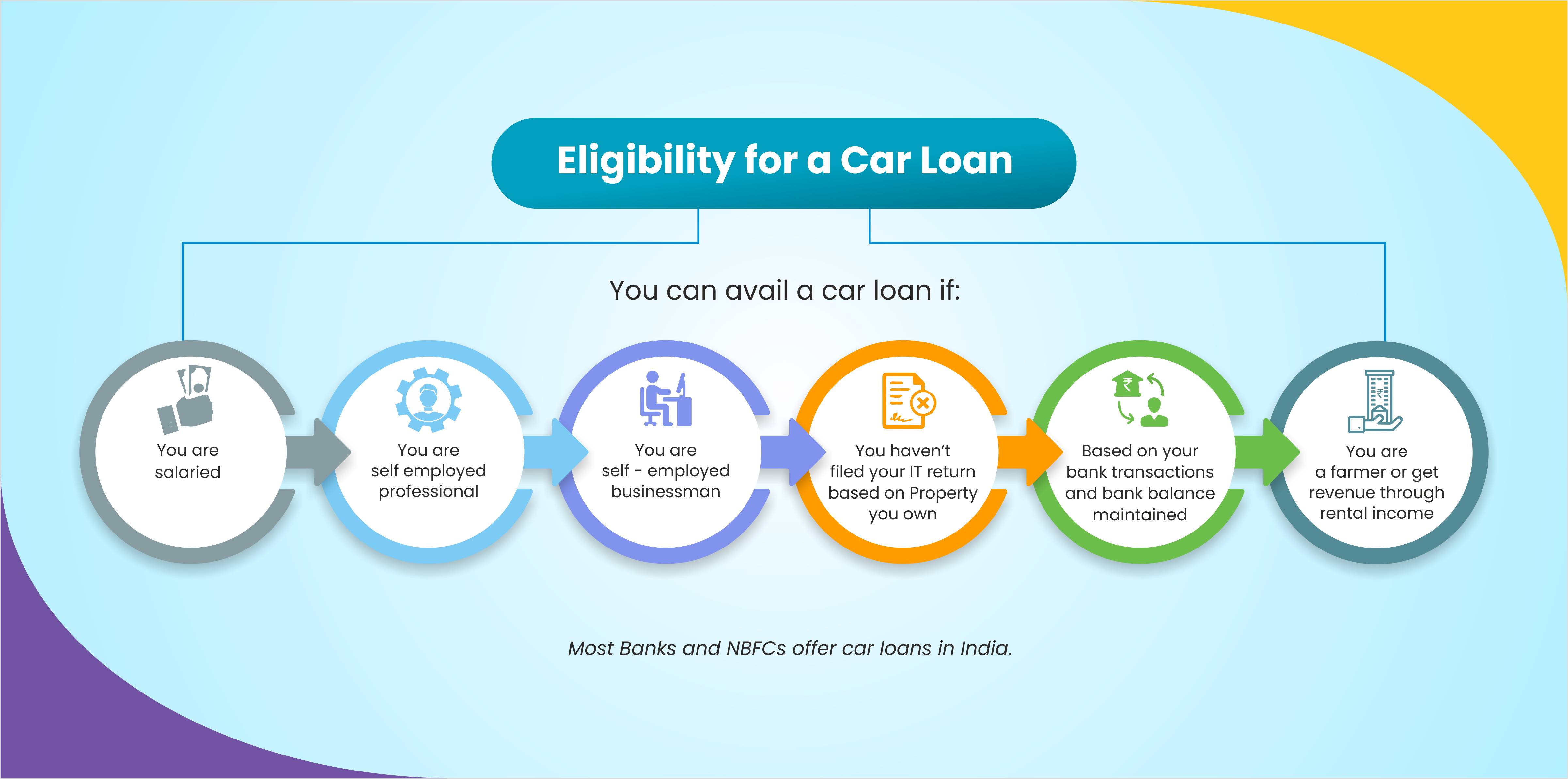

A Car loan is an amount of money borrowed from a lender to buy a new or pre-owned car.

For a new car:

- The interest rate for new cars is very attractive and one of the lowest among all loan types

- Up to 85 to 100% of the car value can be funded as a loan

- Higher the car value, lower the rate of interest

- Tenure ranges from 5 to 7 years

For a pre-owned car:

- Most lenders fund a used or pre-owned car that is at the exit maximum of 8years old (a very few NBFCs fund a car that is up to 10 years old)

- The rate of interest for per owned or used car is 300 to 500Bps* more than that of new cars

- Up to 70% of the car value can be funded as a loan

* 100Bps – 1%

Personal Loan on your existing Car Loan:

You can avail of a personal loan as a top-up on the car loan after 18 months of the purchase of the new car loan. A few lenders fund up to 120% of the car value as a combination of car loan and personal loan

The top-up loan would be at a personal loan rate of 16-18%.

Car Loan Buying Process

For a new car

- Once you decide on which car to buy, you must get the invoice from the car dealer and share it with the banker along with your financials.

- Based on the invoice and your financials, the lender approves the loan and gives a Bankers Cheque (BC) or Delivery Order (DO) to the dealer.

- After receiving the DO or BC, the dealer gives you the delivery/registration date of the car

For a pre-owned car

The process for a pre-owned is a bit tedious compared to a new car:

- For a car without any previous loan

- The process is similar to that of a new car. But before paying the money to the seller, you must ensure that Form 29, Form 30 and Form 28 gets signed, and you must also ensure the insurance transfer documents are taken from the previous owner

( https://parivahan.gov.in/parivahan//en/content/all-forms )

- For a car with a previous loan, the process gets a little tricky

- When you submit the invoice to the lender, you must also submit the loan outstanding letter along with the financial documents.

- Once the loan gets approved, the lender will first give a Bankers Cheque (BC) equivalent to the previous loan amount; you must use this BC to close the loan and get a NOC from the previous lender. After you get the NOC, the remaining loan amount will be disbursed.

- The remaining process is the same as that of a car without a previous loan.

Car Lease

Car lease is gradually gaining more popularity than Car loans as it is a cheaper way of buying a car. Leasing a car is a smart move for any business to optimise its costs. At the end of the lease tenure (2 to 5 years), the car has to be surrendered to the car lease company. If you want to buy the car after the lease tenure, you can bid and pick up the car at the market-linked Realizable Value (RV) or Predetermined or Fixed Realizable Value (RV) at the beginning of the lease contract

In the market-linked RV, whatever is the market value of the car at the time of surrender will be considered. In the fixed RV, the value is pre-fixed at the start of the lease contract

The Car Lease Rental will be charged for an amount equal to the On Road Value of the Car minus the RV agreed at the end of the lease and not at the On Road Value

There are two programmes under-car lease:

- Corporate Lease

Under this programme, A corporate ties up with one or many of the car leasing companies and gives car leasing facilities to their employees. The car can either be in the name of the company or the employee.

The RC card will either have the company’s name or employee’s name on it, while in the Balance Sheet the ownership of the car will be in the name of the leasing company and not on the corporate making it an asset-light proposition

The corporate and car lease company have an agreement wherein the car rental is deducted pre-tax from the employee’s salary. Some of the benefits include:

- It helps the employee save Income Tax when compared to EMI as the lease rental is paid pre-tax

- The leasing company negotiates with the dealer and gets a very good deal

- The leasing company takes care of the insurance by including the insurance amount in the car lease

- If needed by the employee or employer, the lease company can also take care of the maintenance of the car

- MSME Lease

For an MSME, the car lease is an off-balance-sheet item as it is not a loan. The entire car lease amount can be claimed as an expense in the profit & loss, saving Income Tax on it. The minimum turnover of the MSME to get into a car lease should be 10 crores.

The interest rate for a car lease is usually 300 to 500Bps* more than New Car Loan rates but it is still beneficial considering the overall Income Tax saving

Benefits of Car Lease

- Although the interest rate is slightly higher for a car lease when compared to a car loan, the foreclosure charges for a car loan is 5% but for a car lease, it is only 1%

- No hidden extras and fewer overheads

- No down payment for leasing a car

- No risk of resale of the car

- You can lease a car that is more expensive than the one you could afford to purchase

- No check of individual’s credibility

* 100Bps – 1%

We, at aagey.com, have tie-ups with both car loan lenders and car leasing companies. We can offer both car lease as well as car loans at the best possible deal

We, at aagey.com, have tie-ups with both car loan lenders and car leasing companies. We can offer both car lease as well as car loans at the best possible deal

Leave a Reply

You must be logged in to post a comment.